Well, that was a crazy turn of events. Three weeks ago, I thought Parker was going to be acquired in a deal worth nearly $90M. Yesterday, we filed for Chapter 7.

Startup Graveyard — Issue 1: Six founders hit the wall so you can see where it is

Six startup shutdowns dissected for failure patterns — Parker ($200M+ raised, collapsed in 3 weeks), NeoSystems (signed new contracts while preparing to dissolve), NeuroPixel.AI, Rec Room, EO Charging, and Ascend Elements. Each case closes with a diagnostic question for AI founders.

This week's confirmed shutdowns include two direct hits inside the May 5–12 window: Parker (fintech, YC W19) and NeoSystems (GovTech, CMMC compliance). Four additional cases from February through April 2026 — NeuroPixel.AI, Rec Room, EO Charging, and Ascend Elements — are surfaced as pattern context. Together they illustrate five distinct failure modes that show up before, not after, the terminal event.

What makes these cases useful is not the drama. It's the specific sequence of decisions each team made that looked defensible in isolation and proved fatal in combination.

Parker: the deal that died three weeks before Chapter 7

Image from: TechCrunch

Parker, a Y Combinator Winter 2019 company, built corporate credit cards and banking services for mid-market e-commerce businesses. 1 By the time it ceased operations on May 4, 2026, the company had processed over $1 billion in annualized payment volume and reached $65 million in annual revenue.

The headline number — $200M+ raised — deserves a footnote. Of the total claimed funding, approximately $125 million was an asset-backed lending facility, not equity that could absorb operating losses. 2 Equity across the seed, Series A (led by Valar Ventures), and Series B came to roughly $58 million. The $145 million in debt and ABL was collateral-backed, not a cushion.

The collapse was sudden in calendar time but not in structural terms. Parker had gone through leadership turnover, a slowing growth trajectory, and what CEO Yacine Sibous described as "the realities of trying to scale a venture-backed business after momentum fades." 3 Earlier in 2026, the team concluded the best path forward was a sale. They ran a process for months.

That process produced a single serious buyer. On May 9, Sibous wrote on X: 3

Loading content card…

The acquirer, identified as AI tax compliance company Avalara by sources familiar with the situation, backed out at the last minute. 2 When the deal collapsed, Patriot Bank — Parker's credit card banking partner — moved to terminate the card program, even though Parker still had some remaining runway. 2 Chapter 7 (full liquidation, not reorganization) was filed four days later with assets and liabilities each estimated at $50M–$100M.

The morning before the shutdown, Parker's website still displayed its "$200M+ raised" banner. Customers learned about the closure from a Patriot Bank email, not from Parker.

The pattern: a company that survived seven years and $200M in capital ended in three weeks because a single banking partner relationship gave one counterparty the unilateral ability to pull the plug. The M&A process reduced strategic optionality to a single thread. When that thread snapped, there was no fallback.

Sibous said he'd "avoid over-hiring, reactive decisions, and doomsayers" if starting over — but the structural issue had a more specific address: a fintech model that needed Patriot Bank's cooperation to operate at all, and an exit strategy that needed exactly one buyer to say yes.

NeoSystems: signing new clients while preparing to dissolve

Image from: Oxebridge Quality Resources

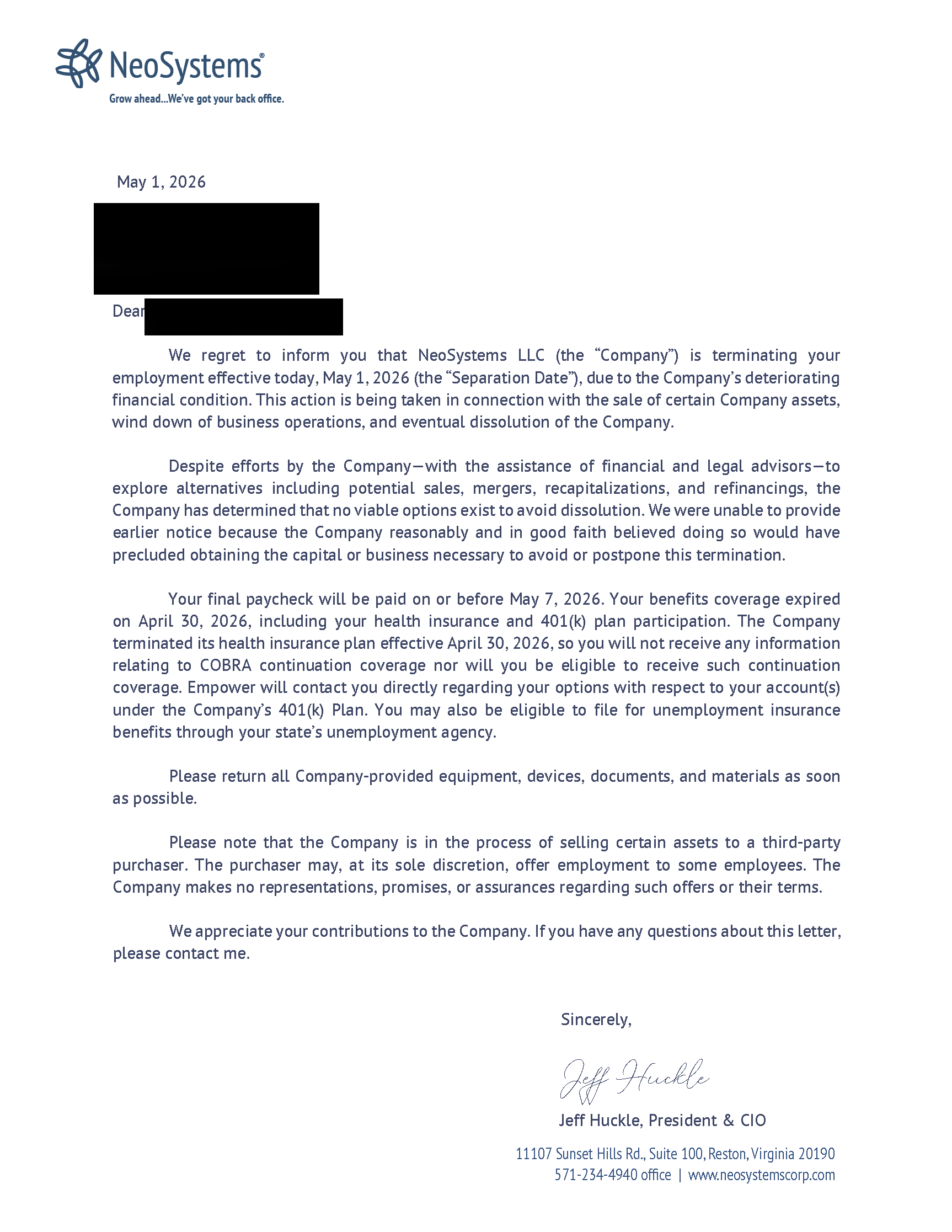

NeoSystems was a Reston, Virginia-based CMMC (Cybersecurity Maturity Model Certification — the Pentagon's compliance framework for defense contractors) consulting and managed services firm. At shutdown, it had approximately 70 employees, held CMMC Level 2 certification, and operated under a GSA Schedule federal government contract.

On Friday, May 1, 2026 at 5:00 PM Eastern, all employees received a termination email signed by President and CIO Jeff Huckle. The email stated the company was "in the process of selling certain assets to a third-party purchaser." 4 Employee health insurance was simultaneously canceled — the company later attempted to walk this back after recognizing the COBRA legal exposure. No clients were notified.

Four days later, Huckle sent an internal message to remaining staff instructing them not to give clients any advice. 4

The company's customer data systems — including CUI (Controlled Unclassified Information) and potentially export-controlled data — were sold to Bluestreet Inc., a buyer that, according to Oxebridge's Christopher Paris, has no apparent CMMC experience. Clients had not been given administrative credentials to their own environments. 4

What makes this case instructive beyond its legal dimensions is the internal timeline that former employees described on Reddit: 5

"They were signing new clients and new contracts as of Monday last week. You don't sign new clients with 12-month contracts knowing you are shuttering your doors, without intentionally trying to defraud the client."

And from a former VP who resigned in August 2025: 5

"I joined NeoSystems during their descent into madness as a VP in August 2025. Three months later, I left after myself and other VPs/Managers reported rampant fraud proliferated across their entire service delivery of 'CMMC services' and were summarily ignored."

CEO Brad Mitchell issued no public statement. The NeoSystems website remained live with full service listings as of May 4. Washington Business Journal reported the closure leaves defense contractors scrambling to maintain CMMC certifications. 6

The pattern: terminal information existed inside the organization — VP-level resignations, internal fraud reports, an asset sale negotiation already underway — while the external-facing posture showed a growing company. The gap between what leadership knew and what clients, employees, and regulators could see was total. That gap is the failure mode, not the financial pressure that triggered it.

For early-stage founders building B2B services businesses: the question isn't just "are we running out of money?" It's "does the information that would change our customers' decisions reach them before the doors close?" NeoSystems' answer, apparently deliberate, was no.

Context: four cases from February–April 2026

The following cases were announced before the primary 7-day window. They're included because they extend the pattern set and fill in structural dynamics that Parker and NeoSystems don't cover on their own.

NeuroPixel.AI: 4 years of AI moat, 6 months of actual edge

Image from: Failory — Too Early To AI

NeuroPixel.AI, founded in Bengaluru in 2020, built AI tools for fashion e-commerce: virtual try-ons, synthetic model generation, and catalog automation. 7 Clients included Myntra, Decathlon, Fabindia, and Van Heusen. Total funding: approximately $1.2M across four rounds, including a Flipkart Ventures seed investment.

In April 2026, CEO Arvind Venugopal Nair announced the shutdown on LinkedIn. His account of why it ended: 8

"While I think we got the broader thesis right (Gen-AI for Fashion) way back in 2021, we got massively outgunned overnight sometime in late 2025. Our product didn't hold up against the capabilities of powerful image generation models like NanoBanana Pro by Google. We had an edge for maybe 6 months out of our 5 year journey."

He continued:

"The game shifted from IP towards distribution quickly — by building layers on top of larger, better models, and we were running on fumes by then."

A compounding factor: "Our biggest client account went under recently, without paying us for over 6 months of work." 8

Nicolás Cerdeira at Failory framed it plainly: "They were not wrong about the trend, they just saw it early. They built real tech for a real problem. And then larger image models got good enough, fast enough, to crush the advantage they spent years building." 7

The pattern specific to AI founders: a 4-year technical head start in computer vision was neutralized within months by a foundation model release. The question "what happens if Google ships a model that does 80% of what we do?" — this is what that answer looks like. The defensibility wasn't durable because it was grounded in model quality, not in data, distribution, or customer workflow lock-in.

Rec Room: 150 million players, $3.5B valuation, still couldn't find the unit economics

Image from: GeekWire

Rec Room, the Seattle-based cross-platform social gaming platform founded in 2016 (originally as Against Gravity), raised $294 million across six rounds and reached a $3.5 billion valuation at its December 2021 Series F. 9 It accumulated over 150 million lifetime players. On March 30, 2026, it announced the platform would go dark on June 1.

The company's own shutdown blog was unusually candid: 10

"Despite this popularity, we never quite figured out how to make Rec Room a sustainably profitable business. Our costs always ended up overwhelming the revenue we brought in... with the recent shift in the VR market, along with broader headwinds in gaming, the path to profitability has gotten tough enough that we've made the difficult decision to shut things down."

The structural problem had been visible for some time. User-generated content (UGC) revenue was growing at roughly 70% year-over-year as of September 2025 — but UGC margins were approximately $0.30 per dollar of sales (after platform fees and creator payouts), compared to roughly $0.70 on first-party content. 9 The faster UGC grew, the more the unit economics deteriorated. AI features introduced in 2025 — including a Maker AI tool for game creation — had per-user AI costs that exceeded subscription revenue from those users.

By March 2025, the company had cut 16% of staff. By August 2025, another 50% of the remaining workforce was eliminated (141 positions). CEO Nick Fajt told the remaining team the company needed to become self-sustaining and couldn't rely on further fundraising — while simultaneously claiming they had runway into 2029. Six months later, he announced the shutdown.

Snap acquired select assets; Rec Room employees moved to Snap's Specs Inc. hardware unit.

The pattern: 150 million users and a decade of operation produced a business that couldn't outlast its cost structure. Engagement was real. Revenue was real. The margin math was structurally broken, and deploying AI features made it worse before anyone modeled the unit economics of doing so.

EO Charging: infrastructure company before the infrastructure market was ready

EO Charging (legal entity: Juuce Limited) was a UK-based company that provided full-service EV fleet electrification — hardware, installation, grid coordination, software, and 24/7 maintenance. Founded in 2014, it deployed roughly 50,000 chargers across 35 countries and counted Amazon, DHL, Tesco, and Uber among its clients. 11 It entered UK administration on April 8, 2026, with PwC appointed as administrator. 12

The company's financial trajectory traced a specific arc: a 2021 Nasdaq SPAC deal at an implied $675 million enterprise value, terminated in March 2022 when growth infrastructure companies became unfundable. An ~$80 million raise from Vortex Energy and Zouk Capital in 2023 funded expansion into the US, Australia, New Zealand, and Italy. PwC identified this overseas expansion as the direct cause of the losses that became unrecoverable. 12

By late 2025, EO had exited the US market, completed a £25 million recapitalization, and narrowed focus to a UK cloud charging platform. A January 2026 M&A process produced no transaction.

Failory's analysis identified the model-level problem: "the business looked scalable on slides, not in depots." 11 Each customer deployment was a custom infrastructure project — unique grid connections, site engineering, stakeholder coordination — that turned EO into a system integrator absorbing everyone else's project risk. Revenue recognition lagged by months. Working capital drained with every new site.

The pattern: the SPAC fell through in 2022 but the expansion plan didn't change with it. The company kept moving as if the capital environment would reopen. It didn't. Infrastructure businesses scale through balance sheets as much as through revenue; when the financing environment shifted, the growth strategy had no contingency.

Ascend Elements: when the factory is the whole thesis

Ascend Elements filed for Chapter 11 bankruptcy on April 9, 2026. 13 The company — founded in 2015 as Battery Resourcers, rebranded in 2022, headquartered in Westborough, Massachusetts — had raised nearly $900 million in investor capital plus $480 million in DOE grants. Its 2023 Series D valued the company at approximately $1.5–1.6 billion.

The core technology, Hydro-to-Cathode, directly transforms shredded battery waste into precursor cathode active material (pCAM) in a single step — a genuine process innovation that had been validated at commercial scale in a Georgia facility. The problem was the flagship Apex 1 factory in Hopkinsville, Kentucky: roughly one million square feet, targeting output for 750,000 EVs per year. At the time of the bankruptcy filing, it was approximately 60% complete. Contractor disputes had reached $138 million. Suppliers had begun filing liens. 14

The external pressures compounded the operational ones. The Trump administration canceled a $316 million DOE grant tied to the Kentucky facility (of which $204 million had already been disbursed). EV market slowdowns led automakers to delay purchasing plans. Chinese battery-material suppliers maintained pricing pressure that compressed margins even before the plant was running. 14

CEO Linh Austin, who joined in March 2025, acknowledged the history on LinkedIn: 15

"When I joined Ascend Elements as CEO in March of last year, I did so with the full knowledge that Ascend Elements had a long history of fiscal and operational mismanagement, and that its future was very much in question."

She described the financial difficulties as "insurmountable" despite assembling a new team and securing over $2 billion in commercial agreements. 15

The pattern: a company attempted simultaneously to operate a recycling business, run lithium recovery, manufacture pCAM, and build a million-square-foot factory — while depending on all four working in concert for the thesis to hold. One factory. No revenue from it. All capital pointed at it. When contractor disputes, subsidy cancellations, and market timing hit at once, there was no decoupled path to survival. The Georgia facility proved the technology worked. The Kentucky facility concentrated all the existential risk.

Five failure modes, five diagnostic questions

Across these six cases, five structural failure modes appear — not as post-hoc rationalizations, but as observable decision patterns that were present months or years before the terminal event.

1. AI moat decay (NeuroPixel)

A specialized vertical AI product built its defensibility on model output quality. A foundation model release neutralized it within one product cycle. The moat was real; it just wasn't durable.

Ask yourself: If a frontier lab released a general model tomorrow that does 70% of what your product does, which customers would stay — and why specifically?

2. Single-thread dependency (Parker)

The company's operational continuity required one banking partner to keep cooperating. The exit strategy required one acquirer to say yes. When both threads ran through the same counterparty collapse, there were no alternatives.

Ask yourself: Which single relationship, if it ended tomorrow, would make your product non-operational within 30 days? What would you do then?

3. Governance opacity masking terminal decline (NeoSystems)

Internal signals of failure — VP resignations, fraud allegations, an ongoing asset sale — were held inside the executive layer while external signals (new client contracts, public credentials, live website) told a different story. The gap between what leadership knew and what stakeholders could see became a liability larger than the financial one.

Ask yourself: What information would change your customers' decisions if they had it? Is there a reason they don't?

4. Unit economics deferred too long (Rec Room)

A platform grew to 150 million users and $3.5 billion in peak valuation without ever finding a margin structure that worked at scale. UGC growth made the economics worse. AI features made them worse still. The company waited for the revenue line to solve the margin problem rather than designing for profitability at a specific scale.

Ask yourself: At your current growth trajectory, do your unit economics improve or deteriorate as the business scales? If you don't know, that's the answer.

5. Single-asset concentration (Ascend Elements, EO Charging)

Both companies built business models in which the central asset — a half-built factory, a custom depot — had to work for anything else to work. No asset, no company. Both faced simultaneous pressure on that asset from multiple unrelated directions (contractor disputes + subsidy cuts + market timing; SPAC failure + international expansion + cost structure). Neither had a decoupled survival path.

Ask yourself: If your primary asset — technology, infrastructure, key partnership, production facility — failed or became unavailable, is there a version of the business that survives?

These patterns don't form a checklist so much as a reading of how the same structural decision-making errors recur across different industries, funding levels, and geographies. Parker raised $200M; NeuroPixel raised $1.2M. Both hit walls that were visible, in retrospect, before the terminal event.

The founders who built these companies were not making random errors. They were making decisions that were defensible given the information and incentives available to them — and then the conditions those decisions depended on changed. That's not a consoling thought. It's a more actionable one.

Cover image from: Failory — The Factory Killed The Unicorn

References

- 1TechCrunch: Fintech startup Parker files for bankruptcy

- 2Fintech Business Weekly: Another Fintech Bankruptcy

- 3Yacine Sibous farewell post on X

- 4Oxebridge: NeoSystems termination letter

- 5Oxebridge: NeoSystems goes out of business

- 6Washington Business Journal: NeoSystems to dissolve

- 7Failory: Too Early To AI

- 8Arvind Venugopal Nair LinkedIn

- 9GeekWire: Rec Room shutting down

- 10Rec Room official blog: School's Out

- 11Failory: One Step Away From Nasdaq

- 12PwC UK: EO Charging enters administration

- 13TechCrunch: Ascend Elements files for bankruptcy

- 14Failory: The Factory Killed The Unicorn

- 15LinkedIn News: Ascend seeks bankruptcy protection

Add more perspectives or context around this content.